The Role of Financing in Therapy: Your Access Guide

TL;DR:

- Financial barriers often prevent people from starting therapy, despite clear evidence that therapy works.

- Exploring options like insurance, private pay, sliding scales, and public funding can make mental health care more accessible and sustainable.

Therapy works. The research on that is clear. But the role of financing in therapy is where so many people quietly give up before they even start. You tell yourself you can’t afford it, or you assume your insurance won’t cover the kind of help you actually need, and the door closes before you open it. That’s the story for far too many people. The truth is, the financial path to therapy is more varied than most people realize. Insurance, private pay, sliding scale fees, HSAs, public funding — each one opens a different door. This guide walks you through all of them.

Table of Contents

- Key takeaways

- The role of financing in therapy: insurance vs. private pay

- When money stress and mental health overlap

- Practical tools that make therapy more affordable

- Public funding and community mental health resources

- My honest take on financing and therapy access

- Start your therapy journey with Mystic

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Insurance has real trade-offs | Lower out-of-pocket costs come with less privacy and limited therapist availability. |

| Private pay offers more freedom | You gain confidentiality, treatment flexibility, and access to specialized care. |

| Financial tools reduce the burden | HSAs, FSAs, and sliding scale fees can cut therapy costs by a meaningful amount. |

| Public funding is expanding | Over $1 billion in recent federal grants is widening access to community mental health services. |

| Financial counseling supports healing | Addressing money stress directly can improve mental health outcomes alongside therapy. |

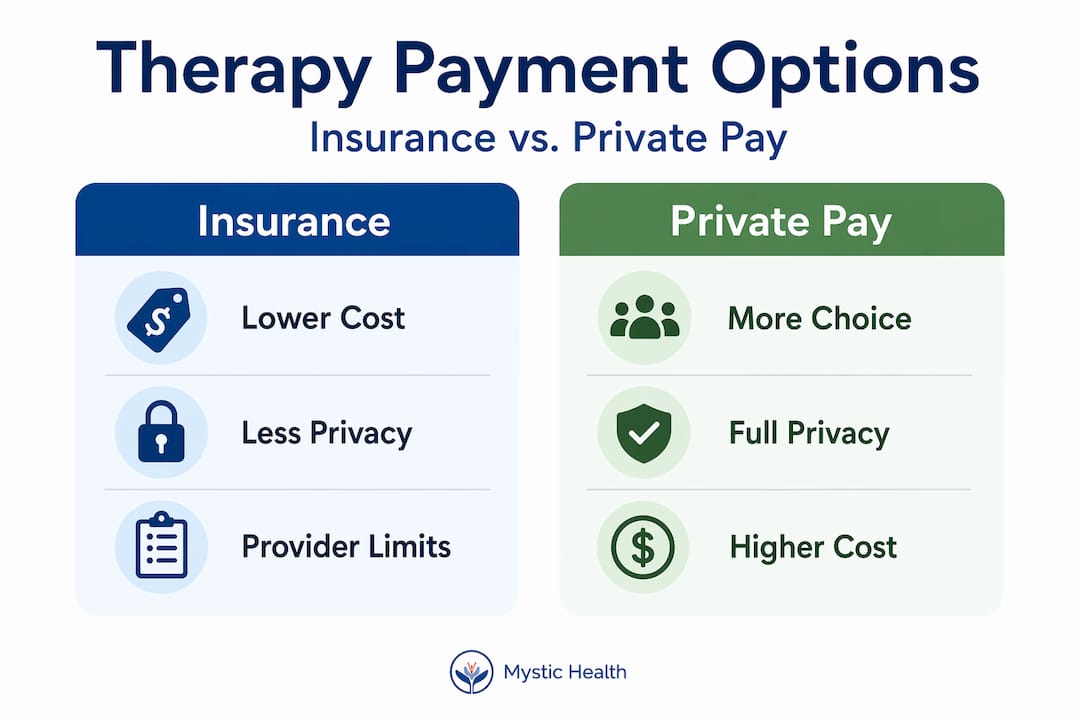

The role of financing in therapy: insurance vs. private pay

The most fundamental split in how people pay for therapy is between using insurance and paying out of pocket. Both paths have genuine merit. Both have real costs you may not see upfront.

When you use insurance, your per-session cost drops significantly. That matters. For someone without much financial flexibility, a $25 copay versus a $175 session fee is the difference between going and not going. But insurance coverage comes with structural limitations that affect who you can see and what kind of care you receive. Many therapists simply don’t accept insurance. compared to $111 on insurance panels, a 43% gap that adds up to roughly $46,000 more per year for a full-time practice. That income difference shapes the market.

The administrative weight on therapists is also significant. Therapists spend 15 to 20 unpaid hours monthly on prior authorizations and billing claims. For many, that hidden cost makes accepting insurance financially unsustainable. The result: a smaller pool of insurance-accepting therapists, longer wait times, and a mismatch between the care you need and what’s covered.

Private pay removes many of those constraints. and modality flexibility that insurance billing rarely allows. Ketamine-assisted therapy, EMDR for complex trauma, psychedelic-assisted psychotherapy — these are the kinds of approaches that fall outside standard insurance coverage. If specialized or integrative care matters to you, private pay is often the only path.

There is also the question of privacy. accessible to insurers and sometimes during life insurance underwriting. If you hold a professional license, security clearance, or work in a field where a mental health diagnosis could have consequences, that record matters. Private pay keeps your care between you and your therapist.

Here’s how the two models compare at a glance:

| Factor | Insurance | Private pay |

|---|---|---|

| Session cost to client | Lower (copay or deductible) | Full rate or negotiated fee |

| Therapist availability | More limited | Broader |

| Confidentiality | Diagnosis on record | Full privacy |

| Treatment flexibility | Restricted by coverage | Open to all modalities |

| Administrative burden | High (for both parties) | Minimal |

A hybrid model, where a therapist accepts a limited number of insurance clients alongside private pay, can be a workable middle ground. It’s worth asking your therapist directly whether they offer this, or whether they can provide a superbill for out-of-network reimbursement.

Pro Tip: Ask your prospective therapist for a superbill. Many insurance plans reimburse 50 to 80% of out-of-network fees, which means you can see a private pay therapist and still recover a significant portion of the cost.

When money stress and mental health overlap

Financial stress and mental health are not separate problems. They feed each other in a cycle that is hard to break without addressing both sides. This is where financial counseling comes in, not as a replacement for therapy, but as something that runs alongside it and makes the healing more sustainable.

, and financial counseling is an important part of the picture for many people. When you can see your finances clearly and make a plan, some of the anxiety that was driving your mental health symptoms begins to settle. That creates more bandwidth for the deeper work therapy asks of you.

A 2022 study showed that online CBT for financial stress leads to significant improvements in depression, anxiety, and perceived financial well-being. This matters because it tells us that the intersection of money and mental health isn’t just about paying for care. It’s about the emotional weight that money problems carry into every session.

Free and low-cost financial counseling options are more accessible than most people know:

- Nonprofit credit counseling agencies offer free or low-fee services and are not trying to sell you a product

- Employee Assistance Programs (EAPs) often include financial counseling sessions at no cost

- Credit unions frequently provide member financial counseling at no charge

- Community Action Agencies offer wraparound services that include financial guidance alongside social support

The goal of financial counseling in the context of therapy isn’t to get rich. It’s to reduce the ambient stress of financial uncertainty enough that you can actually show up present in your sessions, without spending half the hour worrying about how you’ll pay for the next one.

If you understand mental health insurance better before your first session, you can make smarter decisions about which path to take. Mystic’s guide on insurance for mental health covers the details worth knowing before you commit to a plan.

Practical tools that make therapy more affordable

The financing tools available to you go beyond “use insurance or don’t.” Several concrete mechanisms can reduce your actual out-of-pocket cost, sometimes substantially.

-

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs). Therapy qualifies as a medical expense under both. Paying total treatment costs upfront using HSA or FSA funds can leverage a 20 to 30% effective discount compared to paying out of taxed income. If your employer offers an FSA with a use-it-or-lose-it year-end deadline, therapy is one of the best ways to put that money to work.

-

Sliding scale fees. Many therapists quietly offer reduced rates but don’t advertise them. Therapists typically offer two to four sliding scale slots at 50 to 70% of their standard fee. These slots go to clients who need them most. Ask directly and honestly about financial hardship. Most therapists went into this field to help people, and they understand that cost can be a barrier.

-

Payment plans for extended care. Intensive therapy programs, including psychedelic-assisted treatment, often carry higher upfront costs. Many providers, including those in the integrative space, offer structured payment plans that spread costs over three to twelve months. This makes transformative care accessible without requiring a lump sum.

-

Out-of-network reimbursement via superbills. Your therapist submits a superbill, which is an itemized receipt with diagnostic codes. You submit it to your insurance company. Reimbursement rates vary, but many plans cover 50% or more of the allowed amount. It takes some paperwork, but the return is real.

-

Open Path Collective and similar networks. These are directories of therapists who have committed to offering sessions at $30 to $80 for clients with financial need. No insurance required.

Pro Tip: When exploring therapy financing options, always ask your provider two questions before your first session: “Do you have a sliding scale?” and “Can you provide a superbill?” These two questions alone can change what you pay.

Public funding and community mental health resources

The public funding picture for mental health has shifted meaningfully in 2026. Federal investment in community-based mental health programs has grown, and that growth matters for people who need affordable access.

The federal government awarded $794 million in community mental health block grants and $255 million for the 988 Suicide & Crisis Lifeline network in early 2026. That funding reaches community mental health centers, substance use programs, and crisis services across the country. These are real dollars translating into real access, especially in underserved areas.

| Program type | What it covers | Who qualifies |

|---|---|---|

| Community mental health centers | Individual and group therapy, psychiatric services | Low-income, uninsured, Medicaid enrollees |

| 988 Lifeline | Crisis counseling, referrals | Anyone in crisis |

| SAMHSA block grant programs | Substance use, mental health services | State-defined eligibility |

| Medicaid expansion | Outpatient and inpatient mental health | Income-based eligibility |

Medicaid remains one of the most powerful tools for funding mental health services. But it comes with friction. Medicaid expansion enrollees can face cost-sharing up to five times higher under recent policy changes, averaging $542 annually with copay structures. That is a meaningful barrier for people already in financial hardship.

Strategies for getting the most from public funding:

- Check your eligibility for Medicaid or CHIP, especially if your income has changed recently

- Contact your local community mental health center directly, as many offer services regardless of insurance status

- Ask about state-funded mental health programs through your county behavioral health department

- Use the SAMHSA treatment locator at findtreatment.gov to find publicly funded programs near you

The integrative mental health programs that combine modern clinical approaches with community support are worth exploring as this funding picture continues to expand.

My honest take on financing and therapy access

I’ve worked in and around mental health care long enough to know that the financing conversation is usually the one people dread most. They come in hoping to talk about healing and leave with a stack of paperwork. But I’ve also seen what happens when someone finds the right financial path and gets access to the care they actually need. The transformation is real.

What I’ve learned is that the insurance versus private pay debate misses the point for most people. The real question is: what kind of care do you need, and what is the most honest way to make that sustainable for you? For some, insurance is the right answer. For others, especially those pursuing integrative or psychedelic-assisted therapies, private pay with a sliding scale or payment plan is both more flexible and ultimately more effective.

I’ve seen people delay starting therapy for years because they assumed it was out of reach financially. By the time they sorted out the options, they realized they had been one honest conversation with a provider away from getting started. The financing conversation doesn’t have to happen before you reach out. It can happen as part of the intake process.

My advice: don’t let the cost question stop you at the door. Let it be something you figure out together with your provider, because that conversation is part of the care.

— Kabir

Start your therapy journey with Mystic

At Mystic, we believe that financial barriers should not stand between you and healing that actually reaches the root of what you’re carrying.

Mystic Health offers integrative mental health programs that include ketamine-assisted psychotherapy, Spravato, and psychedelic-assisted therapies. We work with patients to understand their financial situation honestly and build a path forward. Our team can walk you through insurance compatibility, financing plans, and sliding scale considerations before you commit to anything. If you’re ready to explore what’s possible, visit our programs and payment options page or schedule a consultation to speak with someone who can help you find the right fit.

FAQ

What is the role of financing in therapy access?

Financing determines who can access therapy, how often, and what kind of care is available to them. Insurance, private pay, sliding scale fees, and public funding all shape whether people can get the help they need.

Why use financing for therapy instead of paying upfront?

Financing spreads the cost of care over time, making extended or intensive treatment programs accessible without requiring a large upfront payment. This is especially relevant for integrative therapies not fully covered by insurance.

Do HSAs and FSAs cover therapy costs?

Yes. Therapy with a licensed mental health provider qualifies as a medical expense under both HSAs and FSAs. Using pre-tax dollars for therapy can reduce your effective cost by 20 to 30%.

What public funding exists for mental health services?

Federal block grants, Medicaid, the 988 Lifeline network, and SAMHSA-funded community programs all provide publicly funded mental health services. In 2026, over $1 billion in new federal funding was directed toward expanding these resources.

How do I ask a therapist about sliding scale fees?

Ask directly and without embarrassment. Most therapists hold a small number of reduced-rate slots for clients facing financial hardship. Simply say: “I’m interested in working with you. Do you offer a sliding scale, and if so, what does your range look like?”

Recommended

Mystic Health Blog

FAQs

1. Am I eligible for ketamine therapy?

2. Does insurance cover the cost of ketamine therapy?

3. How many ketamine treatments will I need?

We recommend two initial treatments to determine suitability and adjust dosage. After these sessions, additional treatments are available based on your progress and specific requirements.